In the high-stakes arena of software buyouts, the silence is often the loudest indicator of impending failure. In April 2026, the industry watched as Thoma Bravo—a titan of the private equity world—effectively handed the keys to Medallia over to its lenders. The transaction wiped out approximately $5.1 billion in equity held by the firm and its co-investors, marking one of the most significant software wipeouts in recent memory.

While the headline focused on the staggering $5.1 billion loss, the real story lies in a quiet, technical mechanism known as the "Payment-in-Kind" (PIK) toggle. For years, this accounting instrument allowed Medallia to mask a fundamental inability to service its debt. With $300 million in annual debt obligations against a backdrop of roughly $200 million in earnings, the company was living on borrowed time—and borrowed interest.

The Mechanism: How the PIK Fuse Works

To understand the current crisis, one must understand how PIK toggles function. Unlike traditional "honest" leverage, where a missed cash interest payment triggers an immediate covenant breach and lender intervention, PIK provides a deceptive bridge. It allows a borrower to defer cash interest payments, instead adding that interest to the principal balance of the loan.

This creates a dangerous illusion of health. The company remains "current" on its debt obligations despite paying nothing in cash. Meanwhile, the principal balance compounds aggressively in the background, growing larger precisely as the business operations begin to deteriorate. By the time the deferral window closes or the loan matures, the borrower is faced with a ballooning debt load that is impossible to service.

This mechanism not only blinds stakeholders to the company’s true health but also degrades the private credit funds (BDCs) holding the debt. Because these funds are required to distribute 90% of their income, they often book deferred PIK interest as real earnings, paying out cash dividends against interest that has never been collected. This charade persists only as long as investors remain quiescent. However, in Q1 2026, the fragility of this system was exposed when non-traded BDCs faced their first-ever quarter of net outflows, with flagship funds from Blackstone and Blue Owl gating redemptions or hitting capital caps.

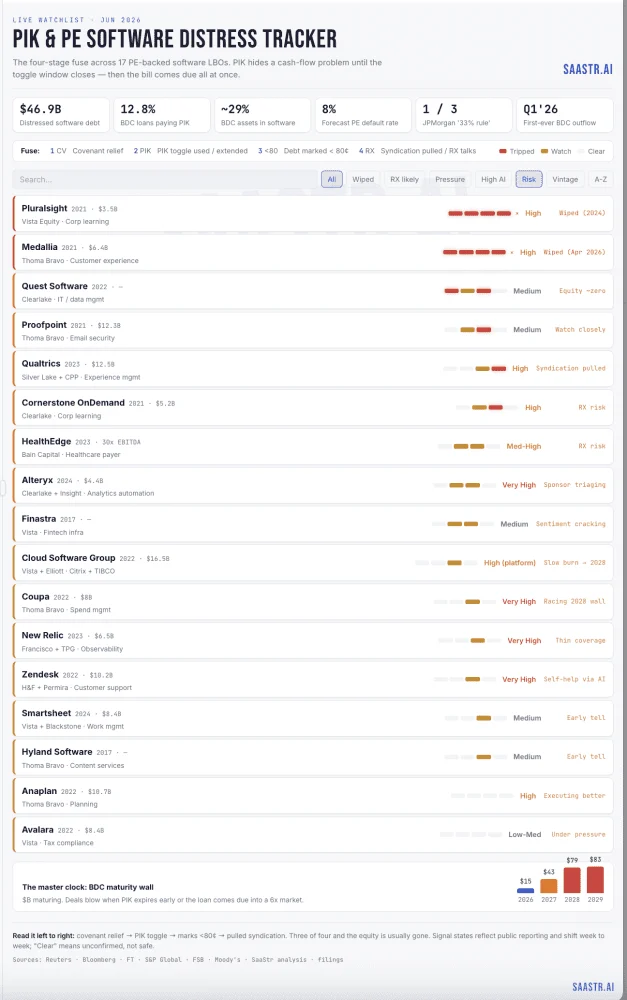

The Backdrop: A $46.9 Billion Distressed Horizon

The Medallia fallout is not an isolated incident; it is a symptom of a systemic "maturity wall" that is rapidly approaching. Approximately $46.9 billion of software debt is currently trading at distressed levels, with $17.7 billion of U.S. tech loans slipping into distress within a single four-week window earlier this year.

Software accounts for roughly 29% of total BDC assets, making it the most PIK-heavy and AI-exposed category in the private credit market. The Financial Stability Board has explicitly noted that the use of PIK toggles serves as a measurable leading indicator, correlating with a 1 to 2 percentage point increase in the probability of loan delinquency in the following quarter.

Financial analysts at Morgan Stanley are now modeling private credit default rates reaching 8%, while JPMorgan’s assessment of the current software book is stark: one-third of the companies will survive as winners, one-third will default, and one-third will become "zombie" entities—existing solely to service their interest burdens until they inevitably collapse.

Chronology of Contagion

The "fuse" for these deals follows a predictable, lethal trajectory. The following breakdown categorizes companies by their proximity to detonation.

Tier 1: Already Detonated

- Pluralsight (Vista Equity Partners, 2021): The "canary in the coal mine." Vista placed over $1.5 billion in private credit debt on the company. By Q1 2023, the firm was already requesting covenant relief and a $75 million equity injection. Despite various maneuvers to keep the entity afloat, including a drop-down transaction to raise new capital, the equity was marked to zero by Q1 2024.

- Medallia (Thoma Bravo, 2021): Bought at 9x forward revenue, Medallia’s demise was accelerated when Blackstone, holding $1.5 billion of the debt, refused to extend the PIK window in late 2025. The company’s inability to refinance at the end of the window led to the total wipeout of $5.1 billion in equity in April 2026.

Tier 2: The Fuse is Lit

- Qualtrics (Silver Lake + CPP Investments, 2023): After a $6.75 billion acquisition of Press Ganey, a JPMorgan-led group attempted a $5.3 billion financing in early 2026. The syndicate pulled the deal due to market fears regarding AI-driven disruption, signaling an immediate and acute liquidity crisis.

- Quest Software (Clearlake): The debt is currently trading at 25 cents on the dollar, signaling that the equity is economically worthless. Formal restructuring appears to be a matter of "when," not "if."

- Cornerstone OnDemand (Clearlake, 2021): With multiple term loans underperforming, Cornerstone is part of a larger, strained portfolio managed by Clearlake, which is currently triaging 11 underperforming companies.

Tier 3: The Clock is Running

- Proofpoint (Thoma Bravo, 2021): With $4.67 billion in debt against $150 million in adjusted EBITDA, this company faces a critical maturity date on August 31, 2028. No covenant relief has been requested yet, but observers are watching 2026 and 2027 for the first signs of stress.

- Cloud Software Group (Citrix + TIBCO, 2022): The largest software LBO by debt volume ($15–$16 billion), the firm faces significant platform displacement risks as Microsoft’s native cloud solutions erode its core business.

- Coupa (Thoma Bravo, 2022): Despite a massive staff reduction, Coupa is racing to re-architect its product for an AI-native market before its 2028 maturity wall.

Supporting Data: The Maturity Wall

The master clock for this crisis is the maturity calendar. Reuters analysis of 74 BDCs reveals a manageable $15 billion in maturities for 2026. However, the pressure intensifies significantly in 2027 with $43 billion maturing, followed by a massive cliff in 2028 ($79 billion) and 2029 ($83 billion).

Because the software market has seen valuation multiples compress from 9x revenue in 2021 to roughly 6x today, many of these companies are unable to refinance. Lenders are currently holding more leverage than they have since the start of the 2023 rate-hiking cycle, making "amend-and-extend" agreements increasingly difficult to negotiate.

Official Responses and Market Sentiment

While private equity firms rarely comment on individual portfolio performance, the secondary market provides a clear, if lagging, signal. Discrepancies between how different lenders mark the same debt—sometimes by as much as 15 points—demonstrate that traditional mark-to-market accounting is failing to capture the reality of the distress. The most reliable signals remain the "upstream" requests: covenant waivers, pulled syndications, and emergency equity injections.

Implications for the B2B Landscape

The implications of this wave of defaults are profound for the broader B2B ecosystem:

- The End of the PE Exit Premium: Private equity is no longer a guaranteed exit strategy at premium valuations. With sponsors unable to refinance their existing books, new acquisitions at 8x–10x revenue are unlikely to clear. Investors and operators should recalibrate their models to 4x–6x multiples.

- The "Debt-Managed" Competitor: PE-backed competitors facing maturity walls in 2027 or 2028 are likely managing toward a debt covenant rather than a product roadmap. This creates a tactical opening for well-capitalized, AI-native challengers to capture market share from firms forced into extreme cost-cutting.

- The Looming Venture Debt Crisis: While the current focus is on massive private equity buyouts, the private credit funds under pressure are closely related to venture debt providers. Startups should assume that if growth slows by even 10–15%, their credit facilities may not be renewed. Proactive communication with lenders is now a competitive necessity rather than a fiscal precaution.

As the industry moves toward the 2028 maturity wall, the "PIK fuse" will continue to dictate the survival of software’s largest players. Those who rely on the silence of deferred interest are increasingly likely to find that silence was not peace—it was the ticking of a clock.