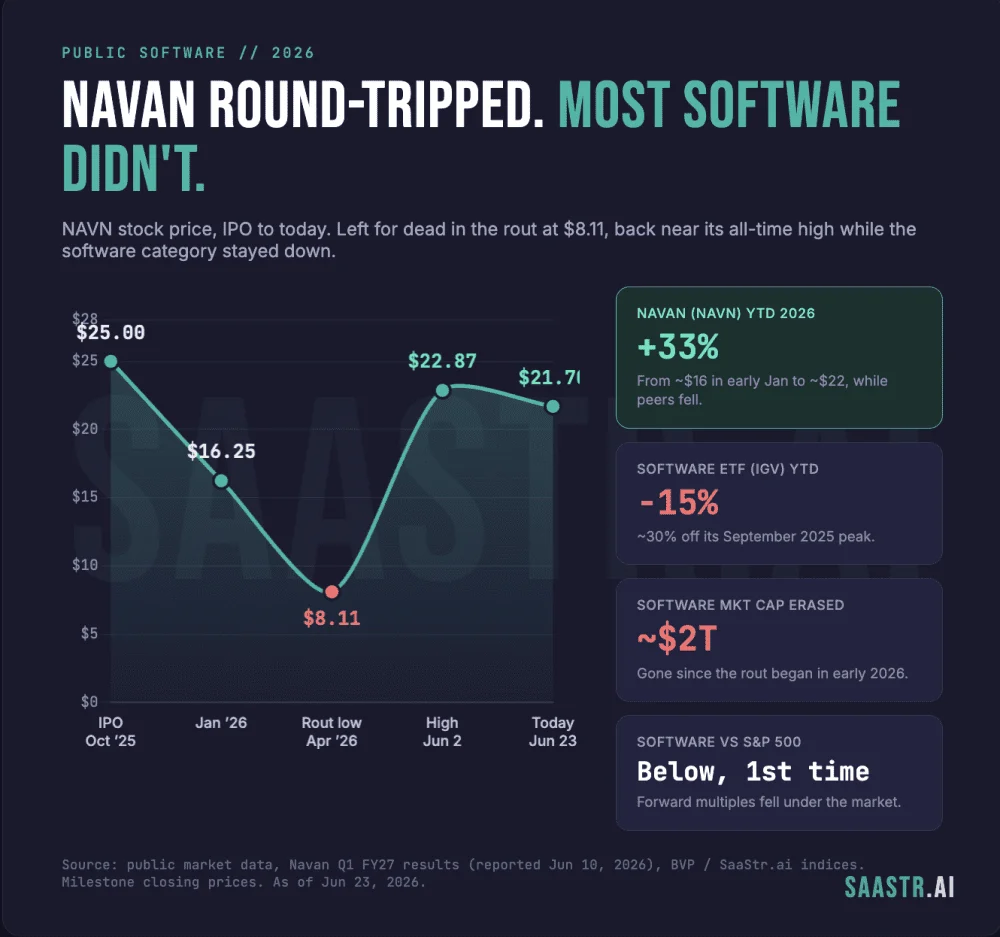

The year 2026 will likely be remembered in financial history as the "Great Software Repricing." For public B2B software companies, the landscape has been a sea of red. The iShares Expanded Tech-Software Sector ETF (IGV) has faced a punishing year, down more than 15% year-to-date and languishing roughly 30% below its September 2025 peak. In a historic first, forward multiples for software companies have dipped below those of the S&P 500, signaling a profound shift in how investors value digital infrastructure.

Amidst this gloom, one company has defied the gravity pulling its peers toward the bottom: Navan.

Formerly known as TripActions, the corporate travel and expense management platform went public in the fall of 2025 at $25 per share, only to be immediately swept up in the worst software market correction since the dot-com bubble. By the time the dust settled on the initial sell-off, Navan’s stock had cratered to a 52-week low of $8.11—a staggering 68% drop from its IPO price. It was, by all conventional market metrics, "left for dead."

Yet, in a display of resilience that few non-infrastructure software companies have managed in 2026, Navan staged a remarkable recovery. Following a stellar Q1 fiscal 2027 earnings report on June 10, the stock surged, hitting a fresh 52-week high of $24.50 on June 11. Analysts at Morgan Stanley, impressed by what they described as one of the strongest prints in their entire coverage group, raised their target price to $33. Today, the consensus rating for Navan is a "Strong Buy," with 13 of 15 analysts backing the stock with top-tier confidence.

A Chronology of the Turnaround

Navan’s journey from a distressed IPO to a market darling was not the result of a lucky break; it was the product of a fundamental shift in its operating model.

The IPO and the Initial "SaaS-pocalypse" (Fall 2025)

Navan entered the public markets at a moment when investor sentiment regarding software was turning toxic. High interest rates and fears that AI would cannibalize the headcount-based revenue models of legacy SaaS companies led to a indiscriminate sell-off. Navan, branded as a growth-stage software company, was caught in the crossfire, with investors punishing it for the perceived risks inherent in its sector.

The "Bottoming Out" (Winter 2025–Spring 2026)

As the company hit its $8.11 nadir, management faced a choice: succumb to the market’s demand for cost-cutting or prove that its business model was uniquely positioned for the AI era. Navan chose the latter, doubling down on automation and proving that its transactional revenue model was not tethered to the "per-seat" vulnerability that plagued competitors like Atlassian and Workday.

The Q1 FY2027 Breakthrough (June 2026)

The turning point arrived with the June 10 earnings report for the quarter ending April 30, 2026. The numbers were not just "good"—they were a rebuttal to the prevailing market narrative. Navan reported revenue growth of 40% and, crucially, signaled a successful transition to profitability with an 11% non-GAAP operating margin. The market, which had been starving for evidence that growth and profitability could coexist, reacted with immediate fervor.

Supporting Data: Why the Numbers Add Up

The catalyst for Navan’s re-rating was its ability to beat expectations while raising guidance in an environment where competitors were doing the exact opposite.

- Growth and Guidance: Navan delivered 40% year-over-year revenue growth. Perhaps more importantly, it raised its full-year FY2027 guidance to a range of $907 million to $913 million. This reflects a projected 30% growth rate—an upward revision from the previously estimated 24%.

- The Power of Volume: Gross Booking Volume (GBV) accelerated by 50%, highlighting that as business travel recovers and shifts toward digital platforms, Navan is capturing an outsized share of the market.

- Operational Efficiency: The company expanded its operating margins by 900 basis points in a single quarter, a feat largely attributed to the successful integration of its proprietary AI agents into the customer service workflow.

The Strategic Moat: Five Core Learnings

Navan’s success offers a roadmap for any business navigating the current software landscape.

1. The Death of the "Per-Seat" Model

The "SaaS-pocalypse" of 2026 is driven by the fear that AI agents will replace human workers. If a company charges by the seat, AI-driven productivity gains become a revenue liability. Navan never used a per-seat model; it charges based on transaction volume (Gross Booking Volume and payment processing). Whether a human books a flight or an AI agent does it, Navan still gets paid. The transaction, not the login, is the unit of value.

2. AI as a Distribution Channel

Most companies view AI as a disruptive threat to their margins. Navan viewed it as a leverage point. By integrating its travel agents with its AI-driven "Cognition" platform, Navan lowered its cost to serve while simultaneously improving user experience. Furthermore, by embedding "Navan Anywhere" directly into Google’s Gemini Enterprise, the company transformed AI into a distribution channel rather than a competitor.

3. Exploiting Competitor Consolidation

The travel industry is filled with "tired" legacy incumbents. When these giants stumble, the market vacuum they leave behind is substantial. Navan reported that 38% of its Q1 customer wins were taken directly from American Express Global Business Travel. When a company becomes the default "modern alternative" in a frozen market, demand generation becomes significantly cheaper.

4. The "Rule of 40" Renaissance

In 2021, the market paid for growth at any cost. In 2026, it demands the "Rule of 40"—the combination of growth and profitability. Navan hit this sweet spot by delivering 40% growth alongside positive free cash flow. This balance is what separates the winners from the companies that are being systematically devalued.

5. Reacceleration is the Ultimate Signal

In an industry where deceleration is the default, Navan’s ability to reaccelerate is its most valuable attribute. By guiding up, the company signaled to the market that its growth is not slowing; it is compounding. This has forced investors to reconsider their valuation models, as Navan has effectively decoupled itself from the industry-wide trend of decline.

Implications for the Future of SaaS

While Navan’s stock has rebounded, the broader reality remains sobering. The median public software company currently trades at a multiple of roughly 3.4x Annual Recurring Revenue (ARR). This is a far cry from the double-digit multiples of 2021. Even for a high-performing company like Navan, which trades at a premium of approximately 6x forward sales, the "ceiling" for valuations has been lowered across the board.

The implications for founders are clear:

- The bar has been raised: To get funded or to achieve a successful exit, showing growth alone is no longer enough. You must demonstrate that your business model is insulated from AI-driven headcount reductions.

- The business model is the moat: As AI becomes a commodity, the way you capture value becomes your only true defensive asset.

Navan has proven that even in a brutal market, success is possible if a company aligns its business model with the direction of technological progress. It did not dodge the AI disruption; it built its house on top of it. For the rest of the software industry, Navan serves as both a benchmark and a warning: in the age of AI, the models that thrive will be those that profit from the automation of the world, not those that rely on the old ways of billing for human time.