In the high-stakes world of vertical SaaS, few companies have managed to marry the brute-force necessity of payments infrastructure with the high-margin elegance of software as successfully as Toast. As of its Q1 2026 earnings report, the company stands at a $6.5 billion revenue run-rate, cementing its position as the dominant operating system for the restaurant industry—and increasingly, the broader retail landscape.

Toast is no longer just a Point of Sale (POS) provider. It is a multi-faceted fintech lender, a high-margin software suite, and, most recently, a rapidly scaling AI agent platform. By achieving durable GAAP profitability while simultaneously maintaining a record pace of expansion, Toast has moved beyond the "growth-at-all-costs" phase to become a blueprint for modern, vertically integrated enterprise software.

The Core Fundamentals: A Financial Inflection Point

The narrative surrounding Toast has shifted from speculative growth to proven profitability. With net income more than doubling to $126 million and free cash flow reaching $115 million in the first quarter of 2026, the company has proven that its complex, three-tiered business model—hardware, software, and payments—can deliver bottom-line results.

Key Performance Indicators

- Revenue Growth: 22% year-over-year.

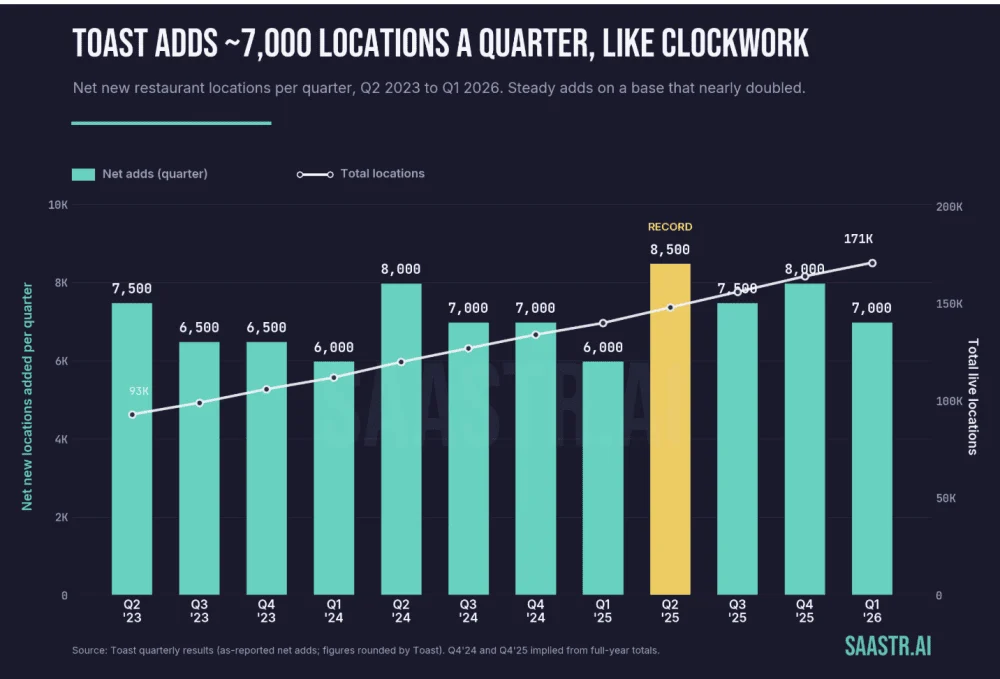

- Scale: Approximately 171,000 live locations.

- Profitability: Crossed into durable GAAP profitability.

- Software Margins: Exceeded 80% for the first time.

- Market Penetration: Over 40,000 locations using AI weekly.

The most telling metric of the quarter was the "take rate." For the first time in its history, Toast’s total monetization across SaaS and fintech exceeded 1% of its $51.3 billion Gross Payment Volume (GPV). This is a critical milestone; it proves that the company’s multi-product strategy—layering capital, analytics, and automation on top of basic transaction processing—is yielding tangible financial returns.

Chronology of Evolution: From POS to AI Powerhouse

Toast’s journey began by solving the most painful bottleneck in the restaurant industry: the legacy, clunky POS system. By digitizing the front-of-house, they captured the "system of record." Once they owned that data, the expansion into payments was a natural, high-margin evolution.

- Phase One (The Foundation): Building the core POS and gaining market share among independent restaurants.

- Phase Two (Fintech Integration): Leveraging transaction data to launch Toast Capital, providing loans to restaurants that traditional banks often ignored.

- Phase Three (Software Upsell): Moving from a utility to a mission-critical software suite, evidenced by the 26% growth in software revenue this quarter.

- Phase Four (The AI Era): Deploying Toast IQ, an AI agent platform that utilizes 14 years of proprietary operational data to automate marketing and inventory management for 40,000+ locations.

This chronology reflects a company that moves with intent. By the time the market became obsessed with AI in 2024 and 2025, Toast already had the data infrastructure required to make AI agents useful, rather than just experimental.

Deconstructing the "27% Margin" Myth

For years, skeptics pointed to Toast’s blended gross margin of roughly 27% as proof that it was merely a low-margin payment processor. However, this headline number obscures a far more profitable reality. Toast operates a "hidden" high-margin software business within a commodity payments wrapper.

The Anatomy of the Margin

- Hardware (The Loss Leader): Toast treats hardware as a subsidized entry point to secure a location. While these units operate at a loss, they are the "hook" that brings customers into the ecosystem.

- Payments (The Volume Driver): This provides the scale. While margins are thinner here, the volume creates the "moat" that makes it difficult for competitors to displace Toast.

- Software/SaaS (The Profit Engine): With margins now exceeding 81%, this is the crown jewel. Software represents only 16% of revenue but contributes a staggering 47% of gross profit.

When analysts strip away the pass-through payment volume, it becomes clear that Toast is, in fact, a highly efficient software enterprise disguised as a hardware-heavy fintech firm.

Strategic Expansion: Moving Upmarket and Outward

Toast’s original success was built on the backs of independent, single-location restaurants. Today, the company is executing a dual-pronged growth strategy: moving upmarket to enterprise chains and moving outward into new verticals like retail and grocery.

The Enterprise Leap

In a stunning display of GTM (Go-To-Market) efficiency, Toast’s Q1 bookings for new enterprise locations exceeded the total customer count of the entire previous year. By landing major accounts like Applebee’s, Alinea, and Preferred Hotels, Toast is signaling that its "vertical playbook"—product depth, local expertise, and seamless integration—is just as effective for massive chains as it is for local bistros.

The Retail Frontier

Retail, specifically the grocery sector, represents the next massive Total Addressable Market (TAM). With over 20,000 independent grocers in the U.S. generating $250 billion in annual sales, Toast is deploying its core platform into a sector that shares the same pain points as restaurants: inventory management, labor scheduling, and payment processing.

The AI Moat: Proprietary Data as a Competitive Advantage

Many B2B companies are currently scrambling to build "AI Roadmaps." Toast, however, is already shipping product. With 40,000 weekly active locations using Toast IQ, the company has moved from theory to utility.

The brilliance of Toast’s AI strategy lies in its "data gravity." Because the company has served as the central nervous system for restaurants for over a decade, it possesses granular, proprietary data on everything from guest ordering habits to labor efficiency.

Why this is a durable moat:

- Operational Context: An AI model trained on generic data cannot optimize a kitchen’s labor-to-revenue ratio. Toast’s models can.

- Integration: The AI agent doesn’t just provide insights; it executes actions within the same system of record that handles the payments.

- Efficiency Loops: The more locations that use the AI, the more the model learns, making the product better for every other customer.

Official Responses and Market Implications

Despite the strong performance, the stock market reacted with a 10% pullback following the earnings print. This reaction serves as a vital lesson in the "pricing for perfection" phenomenon. Even as Toast beat EPS estimates, analysts noted a negative CAC (Customer Acquisition Cost) payback period during the quarter, as sales and marketing expenses briefly outpaced incremental revenue.

Management has maintained a disciplined posture. They are using the savings generated from internal AI engineering productivity to fund the aggressive upsell motion, ensuring that the sales force is not just growing in headcount, but in per-rep output.

The Future of the Vertical SaaS Model

Toast is providing a template for the next generation of SaaS companies. The implications are clear:

- Bundling is back: In a fragmented software world, restaurants and retailers want one "pane of glass" that handles everything.

- Fintech integration is mandatory: Software companies that do not control the payment flow are leaving money on the table.

- Data is the Product: The future of B2B SaaS is not just providing tools for data entry; it is using that data to provide automated, AI-driven decision-making.

Conclusion

Toast has matured from a disruptive startup into a bedrock infrastructure provider. By balancing the "boring" necessity of payment processing with the high-margin, high-growth potential of AI-driven software, they have built a moat that is as deep as it is wide. While the market may punish minor fluctuations in CAC or growth rates, the long-term trend is undeniable: Toast is becoming the operating system for the physical world of commerce. As they continue to push into enterprise chains and retail, their role as the primary intermediary between businesses and their customers is only likely to grow more entrenched.