In the annals of corporate history, growth stories are usually measured in years, if not decades. Rarely does a company emerge from its nascent stages to challenge the very foundations of the software industry in a mere 36 months. Yet, Anthropic—the AI research and deployment company—is currently doing exactly that. With a meteoric rise in run-rate revenue that has left industry analysts scrambling to update their spreadsheets, Anthropic is not just growing; it is fundamentally altering the math of what a software company can be.

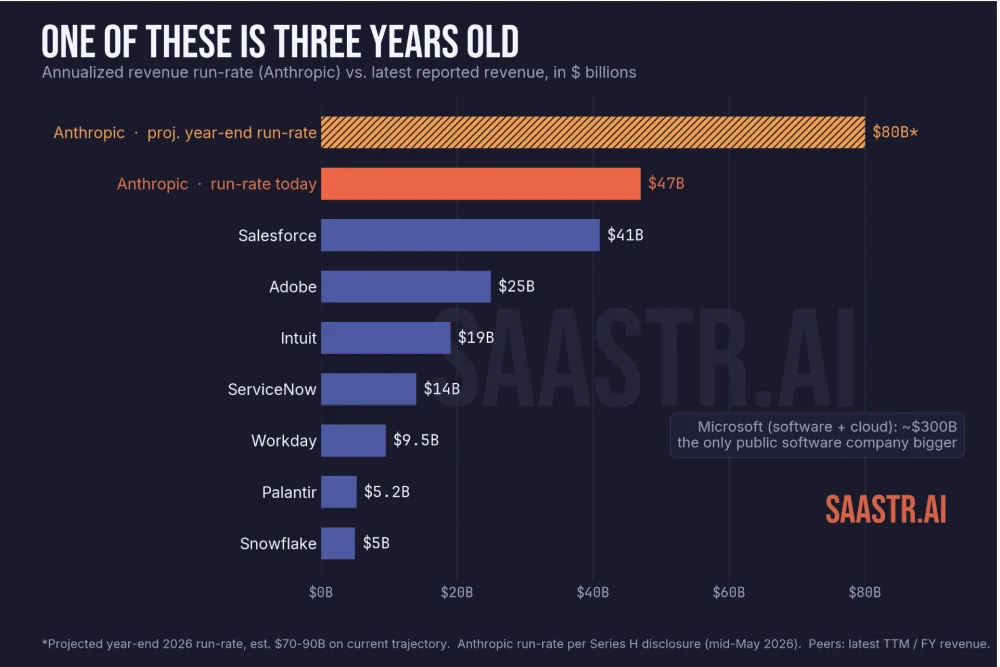

As of mid-2026, the firm boasts an annualized run-rate revenue of $47 billion. To put this into perspective, we are witnessing the fastest scaling of a software entity in the history of the digital age. While the valuation of such companies often dominates the headlines, the underlying revenue data tells a far more compelling—and perhaps unsettling—story for legacy software incumbents.

The Chronology of an Explosion

To understand the sheer velocity of Anthropic’s ascent, one must look at the calendar of the last eighteen months. The figures, disclosed during the company’s recent Series H funding round, represent annualized run-rate—the most recent month’s revenue multiplied by twelve. Because these figures were submitted in the context of high-stakes institutional fundraising, they are subject to intense regulatory scrutiny, ensuring their accuracy.

- Year-End 2025: The company exited the year with a run-rate of approximately $9 billion.

- February 2026: Growth accelerated, pushing the figure to $14 billion.

- March 2026: The trajectory sharpened, hitting $19 billion.

- April 2026: A massive leap to $30 billion, as enterprise adoption of agentic AI hit an inflection point.

- Early May 2026: The momentum continued, reaching $44 billion.

- Mid-May 2026: The official disclosure settled at $47 billion.

This is not a steady climb; it is a vertical ascent. By the time this article reaches the reader, industry projections suggest the company is tracking toward a year-end run-rate of between $70 and $90 billion.

Benchmarking Against the Titans

When holding a $47 billion run-rate against public software giants, the disparity becomes immediately apparent. Anthropic is no longer a "startup" in any traditional sense; it is a behemoth that has eclipsed the annual revenues of nearly every pure-play software titan on the planet.

Consider the landscape:

- Salesforce: Long the gold standard of pure-play software, the company generates approximately $41 billion. Anthropic surpassed this milestone in April 2026.

- Adobe: With revenue hovering around $25 billion, Adobe is effectively half the size of Anthropic’s current run-rate.

- Intuit: At roughly $19 billion, it remains a significant player, yet one that Anthropic has lapped in growth.

- ServiceNow and Workday: With revenues of $14 billion and $9.5 billion respectively, these industry staples are increasingly being dwarfed by the AI juggernaut.

The only entity standing taller is Microsoft, whose sprawling ecosystem—encompassing cloud infrastructure, operating systems, and enterprise software—generates roughly $300 billion. Every other major player, when measured strictly by their software divisions, is now playing catch-up.

The Myth of the "Infrastructure" Counterexamples

Skeptics often point to Oracle and IBM as examples of larger entities. However, a granular look at their balance sheets reveals a different reality. Oracle recently reported $67.4 billion in fiscal 2026 revenue with guidance for $90 billion in 2027. Yet, the core software revenue—the database and application layer—accounts for only $24.5 billion of that total, a segment that actually saw a 1% contraction last year. The remainder of Oracle’s revenue is derived from cloud infrastructure, hardware, and renting GPU capacity to AI labs.

Similarly, IBM remains a $60 billion entity, but its true software footprint is closer to $30 billion. When stripping away consulting and hardware, both companies fall short of the sheer software-generated momentum Anthropic has achieved in just three years of operation.

The Power of Aggregation: A Decade of Winners Combined

Perhaps the most staggering metric is how Anthropic compares to the "next-generation" software class. Investors have long championed the potential of companies like Palantir, Snowflake, CrowdStrike, Datadog, Zscaler, Okta, HubSpot, MongoDB, Cloudflare, and Confluent.

These ten companies represent the cream of the crop in modern software-as-a-service (SaaS). Combined, their annual revenue is approximately $33 billion. Anthropic, as of mid-2026, is generating more revenue than all ten of these industry leaders combined. The largest among them, Palantir ($5.2B) and Snowflake ($5.0B), are being outpaced by the sheer volume of new business Anthropic adds to its run-rate every few weeks.

Financial Nuance: Understanding the "Consumption" Model

Critics may argue that "run-rate" is a forward-looking projection rather than trailing twelve-month (TTM) actuals. It is a fair point: on a calendar-2026 basis, Anthropic will likely realize between $20 billion and $26 billion in actual revenue. This places it in the top five of software companies, not necessarily number two—yet.

However, this distinction ignores the rate of change. The gap between realized revenue and run-rate is the hallmark of exponential growth. Furthermore, Anthropic’s revenue accounting differs from traditional B2B firms. Because it leverages massive partnerships with AWS, Google, and Microsoft, it often books revenue on a gross basis, including the partner’s share as a cost of revenue. While this may inflate the top-line relative to a net-reporting subscription company, it does not diminish the reality of the volume of work being processed.

Implications: The Death of the "Seat"

The most profound takeaway from Anthropic’s rise is the shift in how software is monetized. For the last two decades, the B2B software world has been built on the "per-seat" model—charging customers based on the number of users logged into a platform.

Anthropic has effectively killed that model. It is not selling logins; it is selling tokens and compute cycles. A single developer using an AI agent to refactor a codebase consumes more resources in an hour than a traditional software user might in a year. The success of the "Claude Code" product, which grew from zero to a $2.5 billion run-rate in less than nine months, is a testament to this shift.

The implication for founders and investors is clear: the era of pricing by "user seats" is facing an existential threat. When a company can generate billions by charging for the value of the output rather than the access to the tool, every roadmap based on headcount-driven growth is fundamentally flawed.

The Verdict for the Industry

We are currently witnessing a decoupling of software value from the traditional labor-based model. Anthropic’s trajectory serves as a wake-up call for the entire technology sector. As public software multiples hit decade-long lows, the market is beginning to recognize that the old guard is competing against a model that monetizes output, efficiency, and intelligence at scale.

For the modern founder, the question is no longer whether they can gain market share in their niche. It is whether their pricing model can survive in a market where the largest new software entity on Earth never sold a single "seat." The AI era is not coming; it has arrived, and it is consuming the software industry from the inside out.