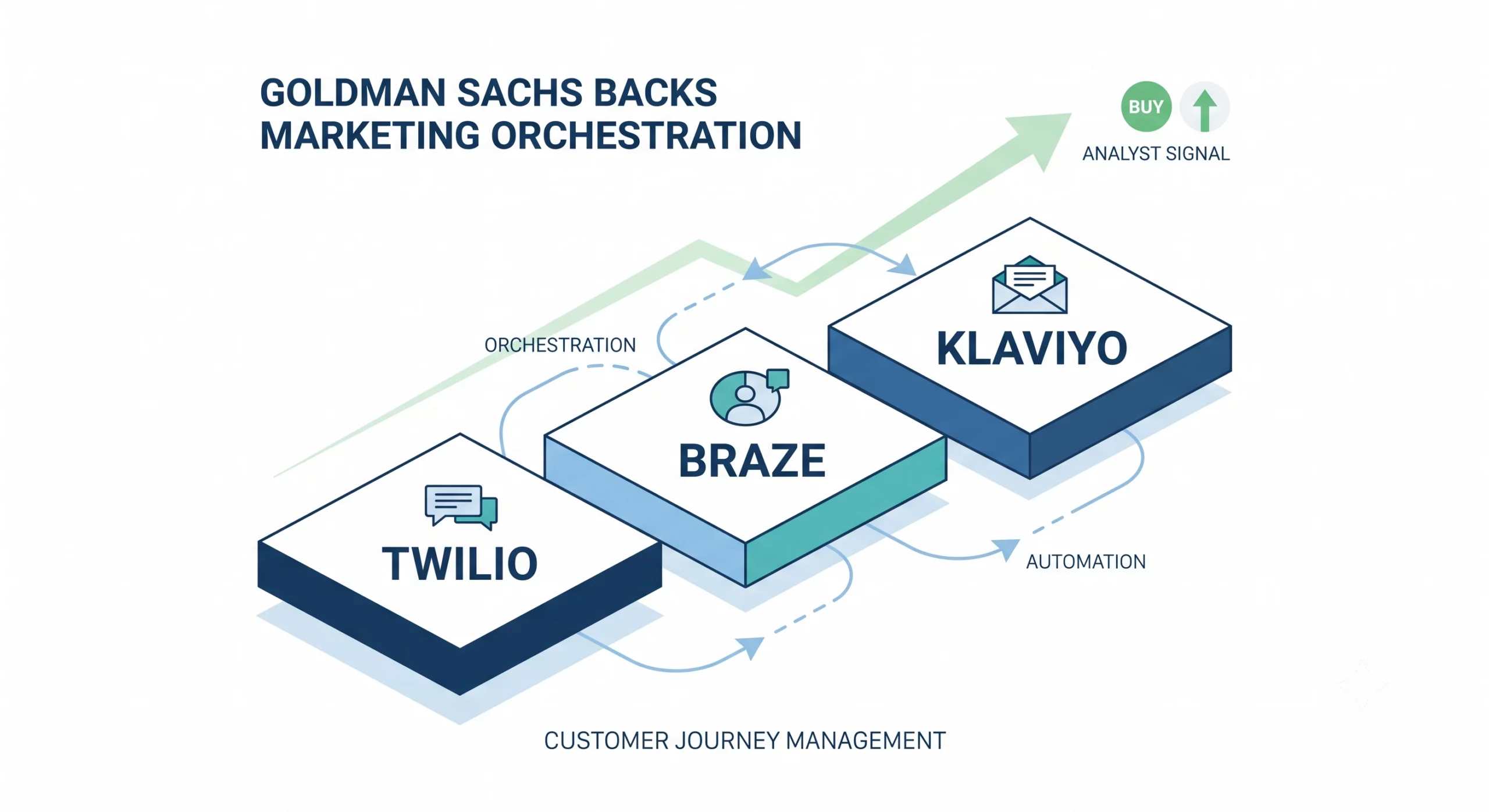

In a significant move that has rippled through the financial markets, Goldman Sachs has issued a sweeping bullish endorsement of the modern marketing technology sector. On Wednesday, June 24, analyst Callie Valenti initiated coverage on four pivotal players in the customer experience (CX) software space, signaling a profound shift in how Wall Street views the intersection of Artificial Intelligence (AI) and digital marketing.

By assigning "Buy" ratings to Twilio, Braze, and Klaviyo—and a "Neutral" rating to Zeta Global—Goldman Sachs is challenging the prevailing "AI bear case" that has haunted these stocks for the better part of the year. The bank’s central thesis is that the market has fundamentally misjudged these companies, erroneously lumping them in with stagnant legacy software providers. According to Goldman, the rise of AI is not an existential threat to these platforms; it is a catalyst for consolidation that favors modern, infrastructure-rich stacks.

The Chronology: A Bold Call Against Market Sentiment

The initiation of coverage comes at a volatile time for software stocks. For months, investors have been wary of the "AI overhang," fearing that generative AI tools might commoditize marketing software, erode pricing power, or allow enterprises to build proprietary solutions, thereby rendering third-party platforms obsolete.

Goldman’s research note serves as a direct rebuttal to this skepticism. The timeline of this move is critical:

- Q1/Q2 2025: Marketing software companies faced significant headwinds. Klaviyo, in particular, saw its shares plummet by approximately 30% following its fiscal 2026 first-quarter results, driven by concerns over decelerating guidance and the sudden departure of its Chief Financial Officer.

- Late June 2025: Amidst a climate of market trepidation, Goldman Sachs stepped in with a definitive contrarian stance. By initiating coverage with aggressive price targets, the bank signaled that the "punishment" meted out by the market—particularly for Klaviyo—has far exceeded the reality of the underlying business fundamentals.

- The Reaction: The market responded immediately to the note, with Twilio shares climbing more than 3% within hours of the publication. The analyst report effectively drew a line in the sand, separating platforms with proprietary, AI-ready infrastructure from those relying on legacy technology.

Supporting Data: The Arithmetic of Upside

Goldman Sachs’ price targets are not merely suggestions; they are projections based on a specific valuation framework that rewards companies currently in the "early innings" of a new product cycle. The disparity between current trading prices and the bank’s targets highlights the depth of the perceived market inefficiency.

Price Targets and Projected Growth

| Company | Price Target | Estimated Upside (at time of note) |

|---|---|---|

| Twilio | $300 | ~63% |

| Braze | $34 | 62%–77% |

| Klaviyo | $26 | ~93% |

| Zeta Global | $28 | Neutral Rating |

The Klaviyo target is arguably the most ambitious. A 93% upside potential implies that Goldman believes the stock is currently trading at an unjustified discount, hovering near its 52-week low. The firm posits that the "bear case"—which characterizes Klaviyo’s deep integration with the Shopify ecosystem as a concentration risk—is actually a fundamental misunderstanding of the company’s strategic distribution moat.

The Strategic Thesis: Infrastructure as the Differentiator

Valenti’s framework for this coverage is built on three pillars: the benefit from AI-driven industry shifts, the ownership of a differentiated infrastructure layer, and being in the early stages of a product cycle.

Goldman argues that "legacy tech debt" is becoming increasingly expensive. As enterprises realize that outdated marketing suites cannot handle the data-heavy demands of AI, they are forced to migrate to modern, modular stacks.

Twilio: The Communications Backbone

Twilio is viewed through the lens of pure infrastructure. As "agentic" AI—AI that can perform tasks and make decisions autonomously—becomes more prevalent, these agents require a way to interact with humans. Twilio’s communications rails serve this exact purpose. With a 20% year-on-year growth in its Voice business and a 28% expansion in its self-service segment, Twilio has cemented itself as the go-to provider for the next generation of AI-enabled enterprises.

Braze: The Momentum Play

Braze is presented as the "cleaner" story in the cohort. Having beaten revenue expectations and raised full-year guidance for four consecutive quarters, Braze is already demonstrating the success of its business model. Goldman highlights the company’s real-time stream-processing infrastructure as a critical competitive advantage, enabling marketers to orchestrate complex, cross-channel campaigns that legacy platforms simply cannot replicate. The bank projects a path to 20% operating margins by fiscal 2029.

Klaviyo: The Contrarian Bet

Klaviyo represents the most significant gamble in the set. The company is currently grappling with a "double whammy": a CFO exit and softer-than-expected guidance. While the market views these as red flags, Goldman views them as temporary growing pains. The bank argues that Klaviyo’s expansion into international markets and its pivot toward customer service cross-selling are being ignored by a market blinded by short-term ecommerce demand concerns.

Implications for the Industry

The Goldman Sachs report is more than just a financial assessment; it is a signal to the entire marketing technology ecosystem. The industry is currently witnessing a stark divergence: modern orchestration platforms are accelerating their growth, while legacy suites are stalling under the weight of their own technological limitations.

1. The Death of the "One Size Fits All" Bear Case

For months, the investment community treated all marketing software as a monolith. Goldman’s selective "Buy" ratings dismantle this view. By assigning a "Neutral" rating to Zeta Global, the bank has explicitly stated that not all modern platforms are created equal. They are vetting the technology, not just the sector. This suggests that future investment will be increasingly concentrated on companies that own their "infrastructure layer."

2. The Shift toward Agentic Marketing

The move underscores the growing importance of "agentic" workflows. As AI transitions from a content generation tool to an active participant in the customer journey, the platforms that control the communication channels—the "rails"—will accrue the most value. This places a premium on companies like Twilio, which are essential for the real-time execution of AI-driven decisions.

3. Capital Allocation and Market Direction

Practitioners and investors should look past the specific 12-month price targets. Instead, the focus should be on the flow of capital. Wall Street is placing its bets on companies that sit closest to the "sending decision"—the moment a brand decides to contact a customer. If Goldman’s thesis holds, we are about to see a massive reallocation of enterprise IT budgets away from legacy marketing clouds and into these agile, AI-integrated platforms.

What to Watch: The Road Ahead

While the Goldman Sachs note provides a strong tailwind for these stocks, the road ahead is not without its hurdles. The success of this thesis relies on several key milestones that must be monitored closely by stakeholders:

- Klaviyo’s Execution: The market will be watching the upcoming quarterly reports to see if the guidance was indeed a conservative reset by management or a sign of systemic demand weakness in the SMB ecommerce space. Furthermore, the search for a new CFO will be a bellwether for investor confidence.

- Braze’s Margin Trajectory: Braze has set a high bar for itself with the promise of 20% operating margins. Investors will be looking for proof that the company can balance rapid growth with increasing profitability as its product suite expands.

- Twilio’s Voice Scaling: As the volume of agentic traffic grows, Twilio’s ability to maintain its growth rates in voice and self-service communications will be the ultimate test of its infrastructure moat.

In conclusion, Goldman Sachs has officially underwritten the thesis that the marketing software industry is undergoing a structural renovation. By framing AI as a filter that separates the agile from the obsolete, the bank has provided a roadmap for where the next cycle of growth in the software sector will likely occur. Whether these specific companies deliver on their ambitious targets remains to be seen, but the direction of the institutional money is now clear.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Nothing contained herein should be interpreted as a recommendation to buy or sell securities. Investors are encouraged to conduct their own due diligence or consult with a qualified financial advisor before making any investment decisions.