Four months ago, the financial markets delivered a brutal verdict on the B2B software sector: the era of the per-seat licensing model was effectively over. In a harrowing 48-hour window this past February, approximately $285 billion in software market capitalization vanished as investors panicked over the rise of AI agents. The prevailing logic was stark and unforgiving—if AI agents can automate the tasks of human employees, the demand for per-seat software licenses will inevitably collapse, rendering the core business model of the enterprise software industry obsolete.

Wall Street dubbed this period the "SaaSpocalypse." The IGV software index plummeted, falling more than 30% from its September peaks and hitting a 52-week low on April 10. At the nadir of the selloff, roughly 75% of software stocks were categorized as technically oversold. While the broad index has since staged a 40% recovery, a distinct divergence has emerged: three of the industry’s most iconic pillars—Salesforce, HubSpot, and Adobe—have been left behind, languishing at or near fresh 52-week lows.

A Chronology of the Disconnect

The narrative of the SaaSpocalypse was built on a clean, testable thesis: AI-driven agentic workflows will replace human headcount, thereby capping the growth potential of companies that charge by the seat. However, as the dust settles, the financial data from the "Big Three" suggests a different reality.

- February 2026: The market experiences a massive, AI-induced selloff, wiping out $285 billion in market cap.

- April 10, 2026: The IGV index reaches its bottom. Sentiment is overwhelmingly bearish regarding SaaS application vendors.

- May–June 2026: Quarterly earnings reports for the Big Three are released. While the market continues to punish these stocks, the underlying fundamentals show a transition toward AI monetization rather than a collapse of the core business.

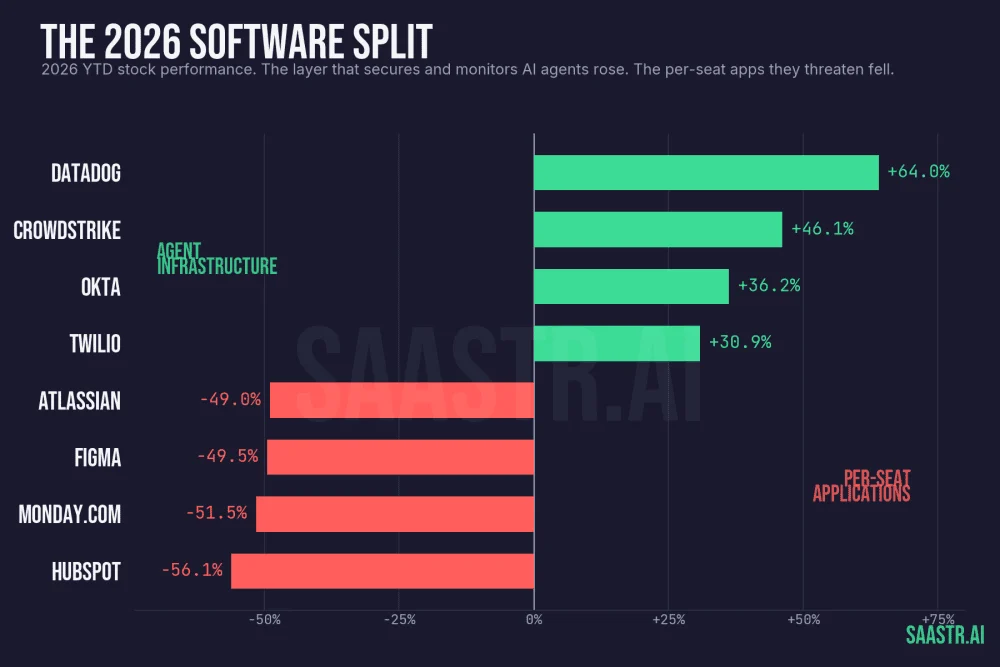

- Late June 2026: While infrastructure-focused companies like Datadog and CrowdStrike hit new highs, Salesforce, HubSpot, and Adobe continue to trade at valuation multiples that suggest the market expects a permanent impairment to their growth.

The Big Three: Fundamentals vs. Perception

The market’s current pricing of Salesforce, HubSpot, and Adobe implies that their core business models are structurally broken. Yet, an analysis of their latest financial performance suggests that the "cannibalization" feared by investors is not manifesting as expected.

Salesforce: The Consumption Pivot

Salesforce, once the face of the CRM revolution, entered its recent earnings print as one of the worst-performing stocks in the Dow. The market had largely written off "Agentforce" as a mere science project. The Q1 FY2027 numbers, however, painted a different picture. With revenue of $11.13 billion (up 13%) and a record 34.8% non-GAAP operating margin, the company demonstrated operational discipline that flies in the face of the "bloated" narrative.

Most significantly, Agentforce ARR crossed $1.2 billion, growing 205% year-over-year. Salesforce has strategically pivoted to pricing these agents by "Agentic Work Units" rather than per-seat licenses. This architectural shift ensures that revenue is tied to output and workflow volume—metrics that can scale even if human headcount within a client’s organization fluctuates.

HubSpot: The High-Growth Paradox

HubSpot has suffered the most violent correction, with shares down over 50% from their 52-week high. Yet, the company continues to report 23% revenue growth and an accelerating operating margin, which hit 17.8% in Q1. HubSpot’s strategy is to layer AI credits on top of its existing seat-based model, essentially creating two monetization levers. With larger, $60K+ ARR deals growing at 64%, the company’s upmarket penetration remains robust. The market is currently valuing HubSpot at approximately 2.5x ARR—a multiple that historically belongs to stagnant legacy businesses, not 20%+ growers.

Adobe: The Complexity of the Transition

Adobe presents the most complex narrative. While the stock trades at its cheapest earnings multiple in a decade, the company faces a dual challenge: a leadership vacuum following a surprise CFO departure and the "freemium" bet on Creative Cloud. Despite these headwinds, AI-first ARR has tripled year-over-year, and Firefly has become a legitimate revenue engine. Adobe’s ability to offer contractual IP indemnification provides a "moat" that free, unverified AI models cannot replicate.

Infrastructure: Where the Market is Betting

While the application giants have been punished, the market has pivoted aggressively toward infrastructure providers. Companies like Datadog, CrowdStrike, Okta, and Twilio have seen their stocks surge, often hitting new highs.

The reasoning is simple: the market is betting on the "picks and shovels" of the AI revolution.

- Datadog benefits as AI models introduce complexity that requires more monitoring.

- CrowdStrike is positioned as the security layer for non-human AI agents.

- Okta is managing the explosion of non-human identity and permission sets.

- Twilio provides the communications pipe through which these agents interact with the world.

These companies do not sell seats that can be replaced by an agent; they sell the very infrastructure that makes the existence of those agents possible.

Implications for the Future of SaaS

The divergence between the application "Big Three" and the infrastructure winners is the defining trend of the current software cycle. The core question for investors is whether the Big Three can successfully transition their revenue models to match the consumption-based success of their infrastructure counterparts.

The Argument for Recovery

If Agentforce continues to scale at triple-digit rates, and if HubSpot’s credit consumption models gain traction, the "SaaSpocalypse" will eventually be viewed as a temporary crisis of perception. Salesforce’s $25 billion share buyback program and its 12% free cash flow yield suggest that management believes the stock is drastically undervalued.

The Risk of Stagnation

Conversely, if the core businesses of these giants continue to decelerate and the AI product lines fail to offset the potential loss of seat revenue, the current discounts will prove to be justified. The risk remains that for every dollar of new AI revenue, a dollar of traditional seat revenue is lost—a zero-sum game that would effectively cap these companies’ growth.

Conclusion: Fear vs. Fundamentals

The current state of the software market is a classic study in behavioral finance. The market has priced the Big Three for structural failure, assuming that AI is a zero-sum replacement for human labor. However, the data from the most recent quarter indicates that these companies are successfully creating "addition"—growing AI-first revenue streams on top of their core businesses.

The "SaaSpocalypse" was triggered by a narrative of total disruption. As companies begin to report their earnings, the evidence increasingly points to a more nuanced reality: the software giants are not being rendered obsolete; they are being forced to evolve their pricing architectures. If the current growth trajectories of these AI-native product lines hold through the next two quarters, the market’s current valuation of these industry icons will likely be remembered as one of the most significant mispricings of the AI era. For now, the disparity between the "winners" and "losers" remains the primary theater of the enterprise software war.