On July 31, 2025, the software industry witnessed a spectacle of pure, unadulterated exuberance. Figma, the collaborative interface design powerhouse, went public at $33 per share. By the closing bell, the stock had surged 250%, settling at $115.50 and commanding a staggering valuation of $68 billion. At its zenith, the stock touched $142.92.

Today, that fervor feels like a relic of a different era. Trading at roughly $19, Figma’s market capitalization has withered to approximately $10 billion—a precipitous 87% decline from its all-time high. It is down 50% in 2026 alone and sits 43% below its initial IPO price. Yet, in a twist that has confounded Wall Street analysts and ignited a fierce debate among institutional investors, the underlying business has not only survived the downturn—it has thrived.

Figma stands as a unique outlier in the annals of busted software IPOs: as the stock price cratered, the company’s revenue growth actually accelerated. This disconnect has triggered a fundamental question: Is Figma the most oversold software asset in the market, or is it a company facing an existential threat that the balance sheet has yet to fully reflect?

The Chronology of a Valuation Collapse

To understand where Figma stands, one must first deconstruct how it arrived here. The "IPO pop" of 2025 was less about price discovery and more about the collision of a tiny float with insatiable market demand. The $142 peak was a sentiment-driven anomaly; much of the subsequent decline represents the inevitable deflation of an overinflated balloon.

However, 2026 brought a more systemic challenge. The broader software sector underwent a violent repricing as investors began to fear that the generative AI revolution would render traditional SaaS business models obsolete. As the index contracted, the companies with the highest valuation multiples were hit the hardest. Because Figma commanded a premium multiple during its 2025 debut, it was disproportionately punished as the tide went out.

The third, and most critical, phase of this decline began in April 2026, when Anthropic unveiled "Claude Design." The market interpreted this launch as an existential signal: if AI can generate functional interfaces from simple prompts, does the world need a design platform? This narrative gained such traction that activist investors, most notably Findell Capital, have begun pressuring Figma’s board to sever its reliance on the very AI labs that now threaten its core business.

Supporting Data: The Reality of the Income Statement

While the market views Figma through the lens of AI-induced obsolescence, the Q1 2026 earnings report, released on May 14, paints a starkly different picture.

Figma is currently operating at a level that qualifies it as a top-decile software business. With 46% year-over-year revenue growth, 82% gross margins, a 139% Net Dollar Retention (NDR) rate, and a 27% free cash flow margin, the company’s fundamentals remain robust. When adjusting for cash on the balance sheet, the stock trades at roughly 6x forward revenue—a far cry from the 30x+ multiples the company enjoyed in 2021.

The data further refutes the "AI-death-knell" theory. If AI were truly cannibalizing Figma, we would not see an NDR of 139%, nor would we see seat expansion across entire enterprise organizations. Most notably, weekly active users of Figma’s "MCP" (the feature allowing AI coding agents to interact directly with Figma files) grew 5x in a single quarter. This suggests that rather than becoming redundant, Figma is evolving into the essential "source of truth" that AI agents require to build software.

Peer Comparison: The Valuation Disconnect

The most compelling evidence that Figma is currently mispriced lies in a comparison with its peers.

The Slow-and-Profitable Anchor: HubSpot

HubSpot serves as the sector’s stable, profitable benchmark. As a 20-year-old category leader in CRM, HubSpot is growing at 18–23% and is expected to generate $750 million in free cash flow this year. Despite having nearly 2.6 times the revenue of Figma ($3.7 billion vs. $1.425 billion), both companies currently command similar market capitalizations of roughly $9–10 billion.

While investors pay a premium for Figma’s faster growth, the valuation gap between the two suggests that the market has lost the ability to distinguish between a mature, cash-generating compounder and a high-growth disruptor. Both are currently trading at "value investor" multiples, yet they have arrived at these low prices through entirely different paths.

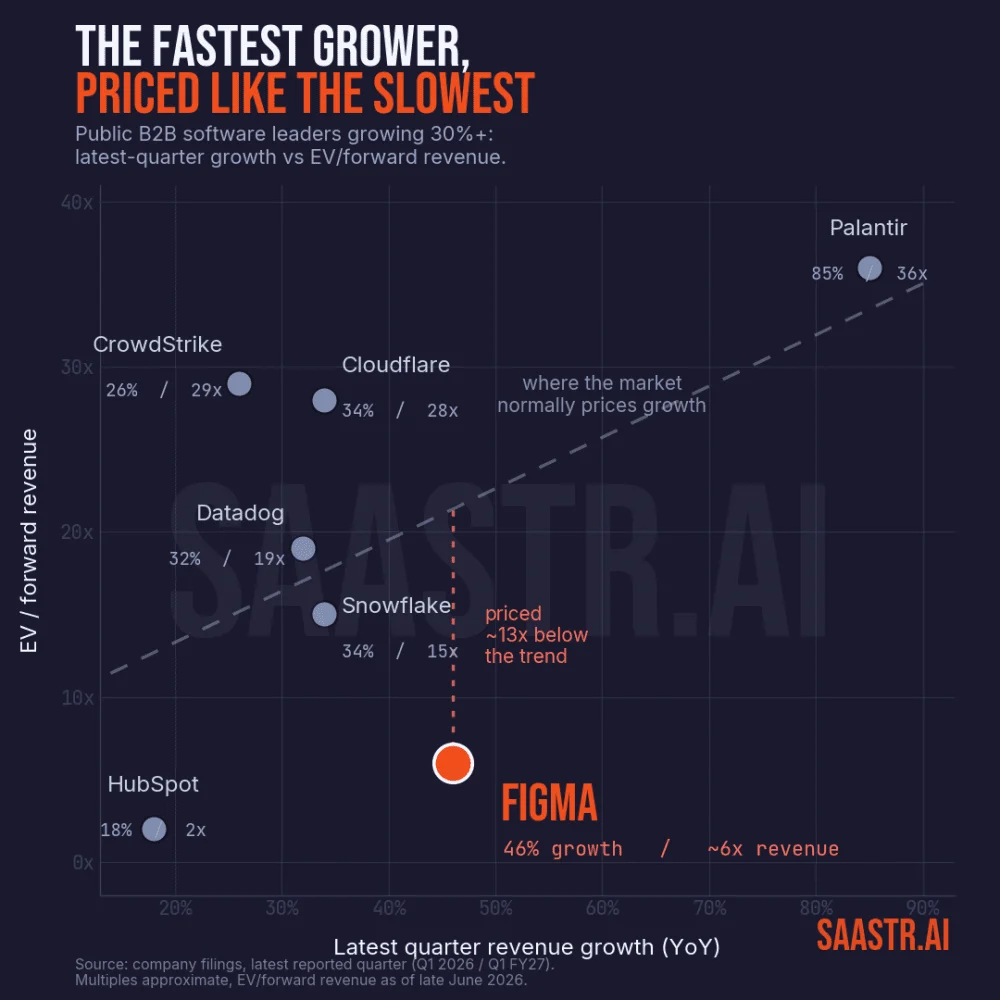

The 30%+ Growth Club: Where Figma Looks Broken

The true anomaly emerges when comparing Figma to other leaders growing at 30% or more. Consider the current multiples (EV to forward revenue) for the industry’s top performers:

- Palantir: 85% growth at 36x multiple.

- Cloudflare: 34% growth at 28x multiple.

- Datadog: 32% growth at 19x multiple.

- Snowflake: 34% growth at 15x multiple.

- Figma: 46% growth at 6x multiple.

Figma is growing faster than every company on this list except Palantir, yet it trades at the lowest multiple of the group, trailing even slower-growing firms. Furthermore, Figma’s "Rule of 40" score (growth rate + free cash flow margin) sits at 73—an elite figure that surpasses Cloudflare, Snowflake, and CrowdStrike. In a rational market, the company with the second-best performance metrics should not be priced with the second-lowest multiple.

Official Responses and Strategic Implications

The boardroom tension is palpable. Activist investors are pushing for a strategic shift, specifically regarding the partnership with Anthropic. The conflict is clear: Figma’s own AI tools are powered by Anthropic’s models, yet Anthropic is simultaneously building products that compete directly with Figma’s core interface design capabilities.

Figma’s leadership faces a classic "Innovator’s Dilemma." They are caught between the need to integrate the best-in-class AI models to keep their product competitive and the risk of empowering a vendor that is also a competitor. The resignation of Anthropic’s CPO, Mike Krieger, from Figma’s board just days before the Claude Design launch, served as a stark reminder of these shifting allegiances.

However, the implications for the broader industry are profound. The market is currently betting on an "Agentic Future" where design is commoditized. The bear case argues that because coding is the primary use case for LLMs, design—which sits just upstream from code—will inevitably be absorbed by prompt-to-interface tools.

The Bull and Bear Thesis: A Conflict of Timelines

The market remains split, with price targets ranging from the high-$30s to the mid-$40s, implying significant upside if the bulls are correct.

The Bull Case:

- Data as Moat: Figma’s 80–90% market share in UI/UX design provides a defensible "system of record" that AI agents need to function reliably.

- Revenue Acceleration: The accelerating growth and high NDR prove that enterprise customers still value the collaboration and precision that only Figma provides.

- Valuation Gap: The current 6x multiple is historically disconnected from the company’s growth rate and elite Rule of 40 performance.

The Bear Case:

- The Gravity of AI: As generative models become more capable, they will allow non-designers to bypass the "design phase" entirely, reducing the need for traditional design seats.

- Resource Asymmetry: Anthropic, Google, and Vercel have deeper R&D pockets than Figma and are iterating at a pace that is difficult for a specialized SaaS company to match.

- The "Wrapper" Risk: If Figma fails to innovate beyond being a "canvas," it risks being relegated to a secondary tool that AI models can route around.

Conclusion: The Signal in the Noise

Figma’s 87% drawdown is not a simple case of a bubble bursting; it is a manifestation of a market that has stopped pricing business fundamentals and started pricing a singular, terrifying macro-fear: that AI will render all software-as-a-service obsolete.

The reality, however, is more nuanced. The next 18 to 24 months will be the proving ground. If Figma can maintain its position as the source of truth for design systems while its users integrate AI agents, it will likely emerge as one of the most significant platform plays of the decade.

For now, the valuation gap remains the most glaring signal. Whether that gap is a temporary pricing error or a rational reflection of an impending death-spiral remains the defining debate of the 2026 software market. The numbers suggest the business is doing just fine; the stock price, however, remains trapped in a future that has yet to arrive.